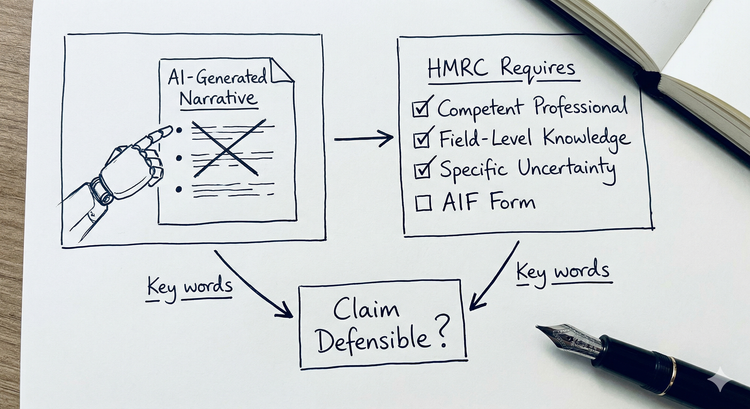

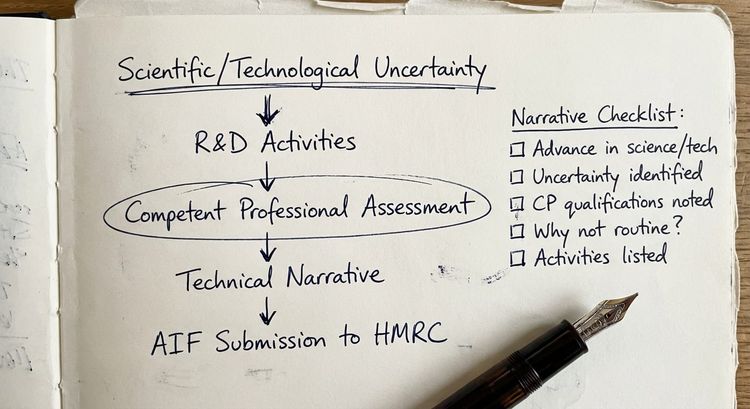

What Is an R&D Technical Narrative and Why Does Your R&D Claim Need One?

HMRC uses your R&D technical narrative to judge whether your claim is credible. Learn what it must cover, who must write it and what a thin one costs you.

2 months ago